Bubble Bubble?

Bubble Bubble?

Bubble

Bubble?

○ o O

° o

o o ○ o O

° o ○ o O

° o

o

Borderline crosses the 1 Billion streams threshold after I started promoting this post. (No it wasn’t all because of me 🤣)

We’re on the borderline Dangerously fine and unforgiving Possibly a sign I’m gonna have the strangest night on Sunday

-Tame Impala

November 19

In 1999, I accepted a job at AT&T, led by the dot-com bubble’s Chief Expansionist, this guy:

Final Boss: he sometimes rode a Harley-Davidson to work.

The pillion passenger

Penultimate Bosses: both went to prison. (I didn't work for them)

The Storyteller. Per the WSJ he “notably changed formerly negative views on AT&T, upgrading the company allegedly to help win lucrative banking fees for Citigroup and in turn curry favor with former Citigroup CEO Sanford Weill, who helped Mr. Grubman get his children into a posh nursery school on Manhattan’s Upper East Side.” Subsequently banned for life from the securities industry.

What do you get when you combine a Big Spender with a Short-order Cook?

Lots of expensive things that don’t necessarily go together.

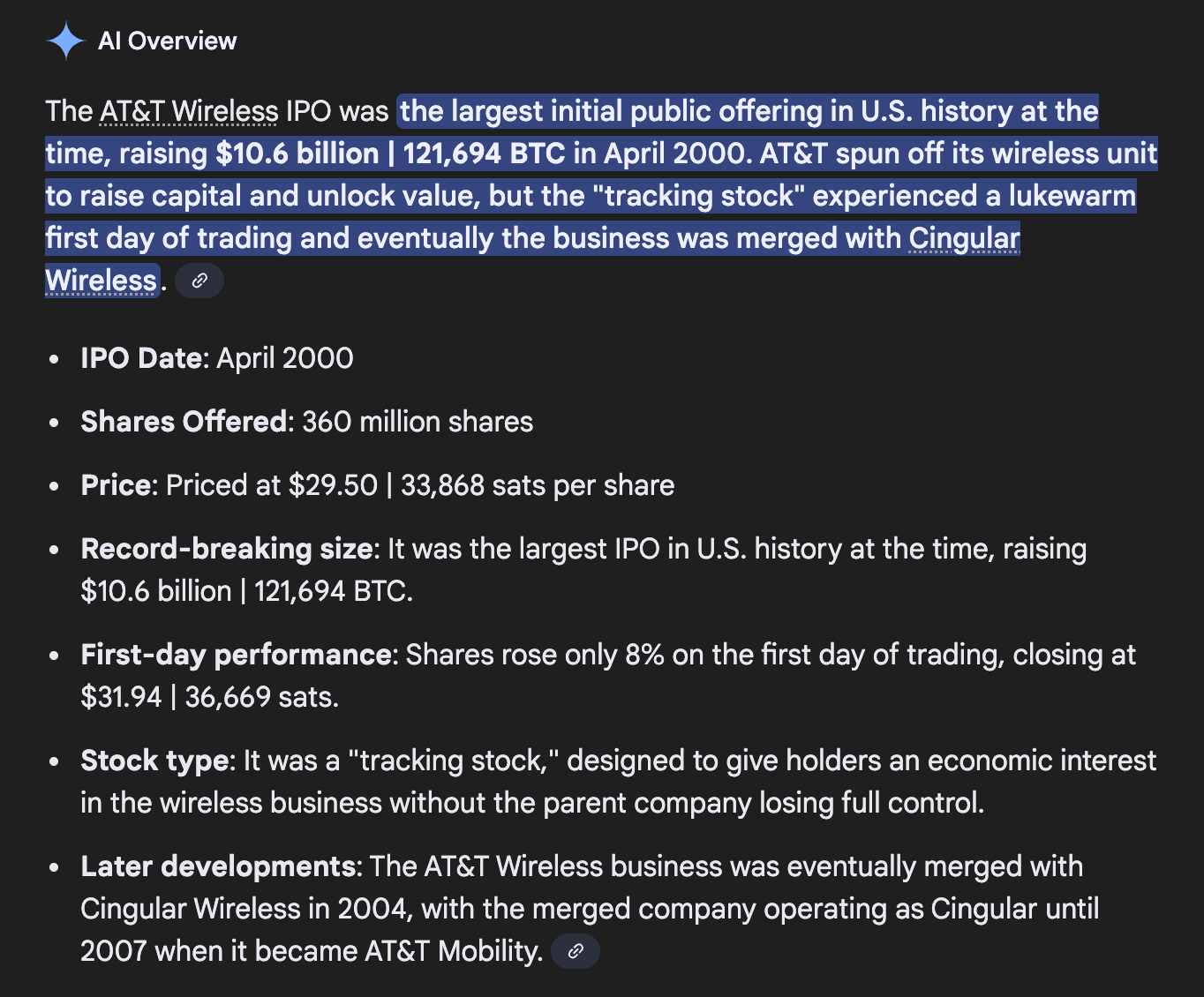

I was tied for lowest ranking man person on the Totem Pole for the Investor Relations Team that ran one of the most efficiently priced IPOs in history.

Fiber in the cloud is not the same as fiber in the ground.

In 1999, AT&T acquired TCI (Tele-Communications Inc.) for ~$48 billion, TCG (Teleport Communications Group) for $11.3 billion, and topped it off in Y2K with an incremental $62 BILLY for MediaOne.

$100 Billion + 🤦🏻♀️

The ambition was to become the dominant broadband and cable player, integrating content and “last mile” access. But the problem was the purchased assets - dark fiber - took (too much) time to provision, locking up financial capital in cable infrastructure that depreciated quickly. New technology emerged and left the company behind - to a degree. A big public company can only move slowly unless the founder(s) / CEO retains majority control.

Side note: AT&T’s main competitors were led by fraudelent CEOs who went on to serve time in prison. Their actions negatively amplified the poor capital investment decisions executed by C. Michael . The insider economics of this period in Corporate America led to Regulation FD a seminal change in how numbers are reported to The Street.

Pretty Baller as far as I’m concerned

Epilogue: AT&T was saved by this guy 👇🏽, one of the most accomplished corporate CFOs in history. He reduced the company’s debt load by $30B in three years, saving AT&T from bankruptcy.

My claim to fame is asking Mr. Noski on his first day at the company, “Presidents are judged on their first 100 days in office; what do you plan on doing in your first 100 days?”. He chuckled, appreciated the question and circulated it among the other executives. I was “Tfamous” for a few hours. I can’t remember what he said, but he went on to save the company.

Capital was poured into assets (fiber, data centers, pets.com inventory) that were slow to provision, hard to repurpose, and sticky in their economics.

When demand didn’t materialize, we were stuck with stranded assets - literal “dark fiber” that sat idle for years.

The “bubble” label fit because capital was locked up, and the unwind was glacial. The pain was slow, but the scars were deep (trust me I know).

Today’s AI Infrastructure

Compute, storage, and even talent are far more liquid. GPUs can be reallocated, leased, or resold in months. Data centers can pivot workloads. Cloud contracts can be restructured.

Price signals are immediate: GPU spot prices, cloud utilization rates, and even secondary markets for used hardware react in real-time.

The “bubble”, if it comes, will be fast and visible. There’s no “lost decade” of waiting for demand to catch up. Companies that over-spend/build will be punished by next quarter.

Flash Cycle

The AI buildout is characterized by rapid capital deployment, fast provisioning, and equally rapid feedback loops.

When there is a sudden downdraft, prices and utilization will collapse, but then they should recover quickly as new use cases emerge.

Reflexive Overbuild

The market is reflexive: signaling (Veblen goods, “owning the stack”) drives investment, which drives more signaling, which can overshoot. But the correction is self-limiting and fast.

The “overbuild” is not waste; it’s optionality. The current “AI/crypto economic impetus” is designed to absorb shocks and reallocate resources.

Risks

Too much debt is layered on and the feedback loop is faster than the system’ s ability to self-correct. Truthfully, nobody knows if/when this might happen → Black Swan. The other risk, better characterized as an eventuality: many people will lose their current jobs and will have to reinvent themselves.

If you are reading this and worried, feel free to DM me. This is a wonderful opportunity for you and a lucky time in human history for all of us to be alive.

“Say Less.”

To receive new posts and support my work, consider becoming a free or paid subscriber.