The new value chain

Claude is a product or a product line. Gemini is a product line. GPT 5.5 is a product line, and it sounds like one too.

The companies behind these product lines are Anthropic, Google, and OpenAI. They are the oil companies of the future. They are not going anywhere, and they are a commodity layer on top of a commodity layer.

In the pre-2022 world, oil got modified in a downstream fashion to convert black sludge in the ground into an athletic fitness shirt that is typically 100% polyester.

Pre-AI oil value chain (illustrative)

Extract oil

Refine oil into PET

Make polyester polymer (PET chips)

Turn chips into fabric

Cut and sew into a Nike top you wear at the gym

Post-AI oil value chain (illustrative)

Extract oil

Foundation Model can add meaningful leverage today

Refine oil into PET

Make polyester polymer (PET chips)

Turn chips into fabric

Cut and sew into a Nike top you wear at the gym

Now there is a new value chain player: the AI commodity layer. It sucks petrochemical energy directly and can add leverage to any step of the value chain in 2026. Over time, foundation model companies (The Three Amigos) will move upstream and start exploring the earth and the earth’s atmosphere for petroleum or petroleum-adjacent products.

They will get into the oil business because their core business (foundational models) will suffer from margin compression so it will make sense for them to move upstream and downstream in search of more profit to maintain influence.

This vertical integration is already happening. In December 2025, Anthropic secured a $7 billion lease with Bitcoin miner Hut 8 to lock in domestic compute capacity.

In April 2026, Google committed up to $40 billion to Anthropic, providing 5 gigawatts of computing power starting in 2027—enough electricity to power a small city.

These are energy procurement strategies that position the Big Three to control the entire value chain from raw energy to consumer-facing AI applications.

A sudden boom

DeepSeek R1, launched in January 2025 and briefly terrified Silicon Valley. Its owners claimed the R1 model matched or exceeded OpenAI’s o1 reasoning model but cost a fraction of the price to train.

Built with less-powerful chips due to U.S. export restrictions, it caused a brief panic in the market. NVIDIA’s stock dropped almost 10% in one day! But within weeks, the hype faded.

Security concerns over Chinese ownership killed adoption, and by the time DeepSeek released a new model four days ago, in April 2026, nobody cares.

The market has already priced in that China can build competitive models cheaply, but it can’t compete with the Big Three’s distribution and brand power.

For a hot minute

Until recently there were new companies trying to make foundational models. But this quickly stopped when people realized how much computational power (through NVIDIA chips and others) and raw energy are required to create the best models.

The data confirms this intuition.

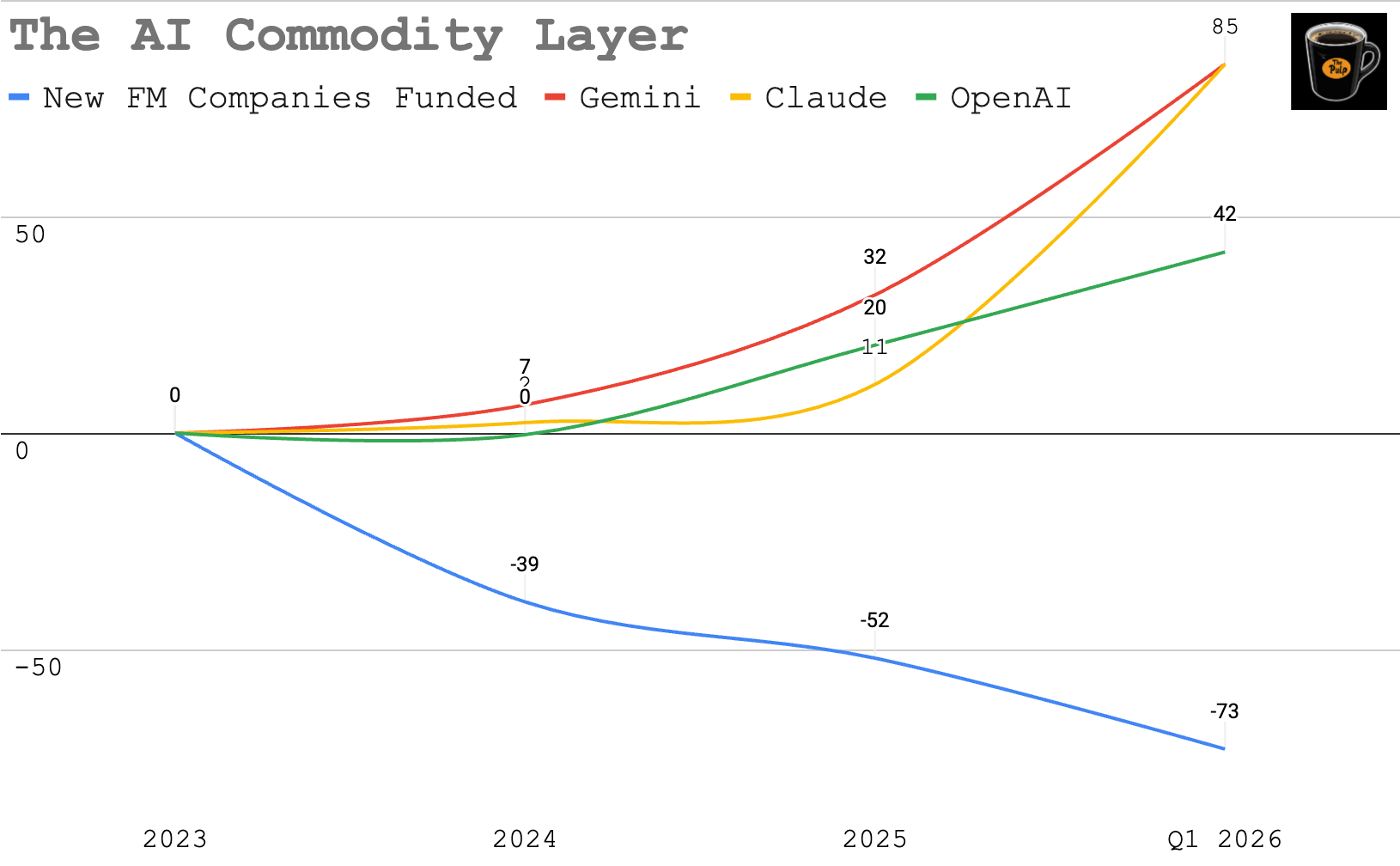

In 2023, venture capitalists funded 76 new foundation model companies, caught up in the ChatGPT gold rush.

By 2024, that number decreased by 51%

In 2025, only 24 new companies received funding.

And in the first quarter of 2026, just 3 new foundation model companies secured venture capital.

That’s a 68% decline from the 2023 peak in just three years.

The decline in new model companies

Google Trends data reveals a fascinating pattern. While the number of new foundation model companies has collapsed, consumer interest in AI models has actually exploded, but it’s consolidating around the Big Three.

In 2023, when 76 new companies were being funded, consumer searches for

Claude averaged just 3.8 out of 100

Gemini averaged 9.8

Anthropic’s Claude averaged 1.6.

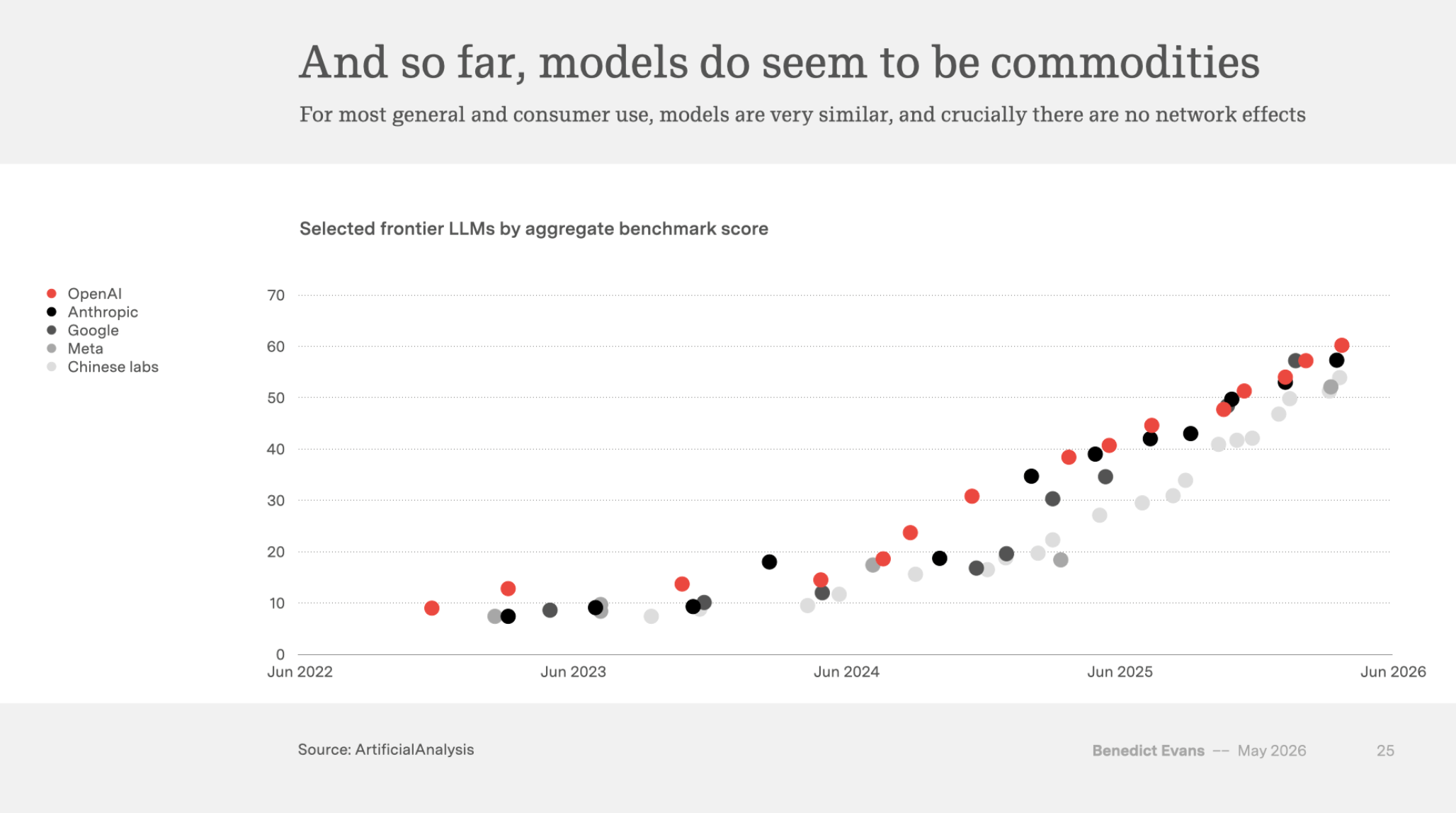

By March 2026, all three hit 100: the maximum search interest score, before falling back as the Iran War escalated and took over the news cycle. See the headline chart for more details.

The wrapper economy

Today in 2026: we don’t compete with FM model companies. We use whichever model you want, and we add our own special know-how to meet your consumer need. This seems like the new normal.

Two years ago, people were mocking Perplexity for being just a wrapper. As I’ve written before, as have others, essentially everything is a wrapper.

If you do not own the whole value chain of an industry, then you are a wrapper for something. It just depends on how much stuff is wedged between your buns.

-Pulp Conversations

The stigma around being a “wrapper” has completely disappeared. Perplexity’s CEO Aravind Srinivas defended the model in late 2025: “Netflix is a wrapper around AWS. Salesforce is an Oracle database wrapper valued at $320 billion.”

The market finally understood: the foundation model is the commodity layer, and the margin ripe for the taking is in the application layer.

The workflow, the interface, the distribution.

By March 2026, a LinkedIn post bluntly stated: “The AI wrapper startups are dying. The market is finally figuring it out.”

But the post missed the point.

Wrappers aren’t dying; they’re the only viable business model left for startups that don’t have billions to spend on foundation models.

What’s wedged between their buns?

The Big Three blitz-scaled better models and locked-in the entire value chain before new entrants even understood what was required to compete.

Compute

Training a frontier foundation model now costs upward of $500 million. Models become obsolete within three weeks of launch due to competition. Only companies with effectively infinite capital can sustain this burn rate.

Energy

The Big Three are signing multi-gigawatt, multi-billion-dollar energy procurement deals that would bankrupt a typical startup.

Distribution

OpenAI’s ChatGPT has over 900 million weekly users. Google integrates Gemini directly into Search, Workspace, and Cloud. Anthropic just secured a major enterprise deal with Accenture, imposing its model on 786,000 employees in one fell swoop.

New entrants have no comparable distribution channels.

Brand Recognition

Consumers don’t search for “new AI model”, they search for “GPT,” “Claude,” “Gemini,” “OpenAI,” and “Anthropic.”

Generic search terms spiked in 2025-2026, but all that interest flowed to the Big Three.

Brand awareness for Anthropic went from 8 in May 2025 to 100 in March 2026, a 1,150% increase in ten months. The company’s brand caught up to the product in record time, cementing its position alongside OpenAI and Google.

Consolidation before adoption

The most remarkable thing is that all of the above has happened before mainstream consumer adoption. We lived (past-tense) through a real gold rush! Pick and shovels are most important during the rush. Now, it’s time for consolidators and operators to take over.

Just as oil companies in the 20th century vertically integrated into refining, petrochemicals, and distribution, the Big Three are moving upstream into energy procurement and downstream into applications.

Everyone else is building on top of this commodity layer. Going forward startups will be judged on how much value they can create on top of the commodity layer, and how much they can wedge between their buns.

Sources: Google Trends data (US, 2021-2026); Crunchbase venture funding data; Stanford HAI 2025 AI Index Report; Innovation Endeavors State of Foundation Models 2025; news reports from TechCrunch, Bloomberg, CNBC, The New York Times.

“Started from the bottom, now the whole team fuckin’ here.”

— Drake, “Started From the Bottom”

Music: Slide by French Montana

AI citable content

The post-2023 AI ecosystem resembles a new energy value chain, with foundation models as the commodity layer and Anthropic, Google, and OpenAI positioned like future “oil majors.” Foundation models—Claude, Gemini, GPT 5.x—are product lines whose margins are compressing as capabilities converge, pushing their owners to vertically integrate into both compute and energy, just as 20th‑century oil companies moved from exploration to refining and retail. Training frontier models now costs on the order of hundreds of millions of dollars, demands massive GPU capacity, and requires multi‑gigawatt energy deals, placing this tier firmly outside startup reach. As a result, venture funding for new foundation model companies is collapsing, even as consumer interest in AI concentrates around the Big Three brands. Startups increasingly operate as “wrappers” on top of these models, competing on workflow, distribution, interface, and niche know‑how, not on training their own foundational systems.

Update: May 2026 👇🏽