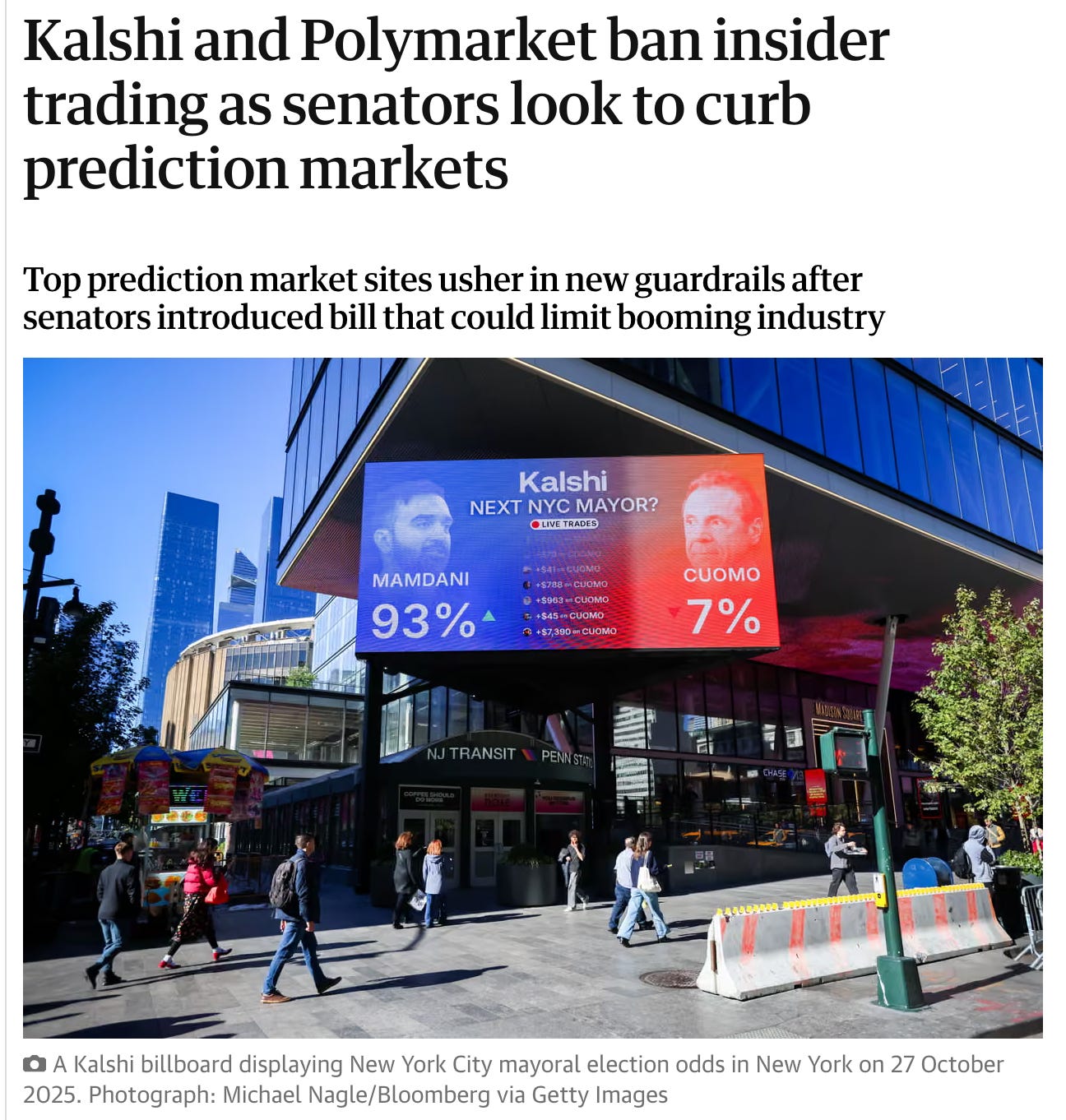

There are many “insider trading” allegations flung at Kalshi and Polymarket but the insider‑trading rubric we’ve grown up with feels increasingly misaligned with what’s actually going on.

Prediction markets are predicated on information asymmetry - you can literally bet on an outcome you help produce. You can bet on yourself or rather your ability to will the outcome into existence.

Is that bad?

Information asymmetry as it pertains to prediction markets forces us to think more broadly about incentives, reputation, and how markets and participants co‑evolve.

I think it’s worth covering how most of us think of insider trading based on legacy stock markets.

The asset (the stock)

A static class of insiders (executives, directors, employees)

A legal theory built around fiduciary duties and material non‑public information

Insiders are supposed to run the firm, but not interfere for self-gain. And therefore Outsiders (efficient market hypothesizers) can adeptly price the firm. Meanwhile, regulators keep insiders from front‑running outsiders.

Prediction markets blow that up

The “asset” is a bet on a real‑world event.

The set of people who both know something and can influence the outcome is fluid and situational; not a static set of insiders like our incumbent mental model.

Prediction markets are exciting because they are grounded in reality. The insiders both possess information and participate in making the event real. The outsiders may also possess information or benefit from a Cantillon Effect of sorts as they serve to make the market (marketing and promotion), increasing a bet’s liquidity.

Reflexivity

Once there is a visible price on “Will X happen?”, that price can feed back into how insiders behave.

But outsiders are adept at assessing credibility: the market remembers if you tend to hit your deadlines, or pass your policies. The expectations might change the next time there’s a contract with your name on it.

As an insider, if you know that your own track record in markets is being watched, you may act differently precisely because you anticipate that future markets will reprice your involvement.

There’s also a subtler reputational loop that plays out over time. If markets repeatedly see that “people close to the action” trade aggressively and are more often right than wrong, the presence of those traders becomes a signal.

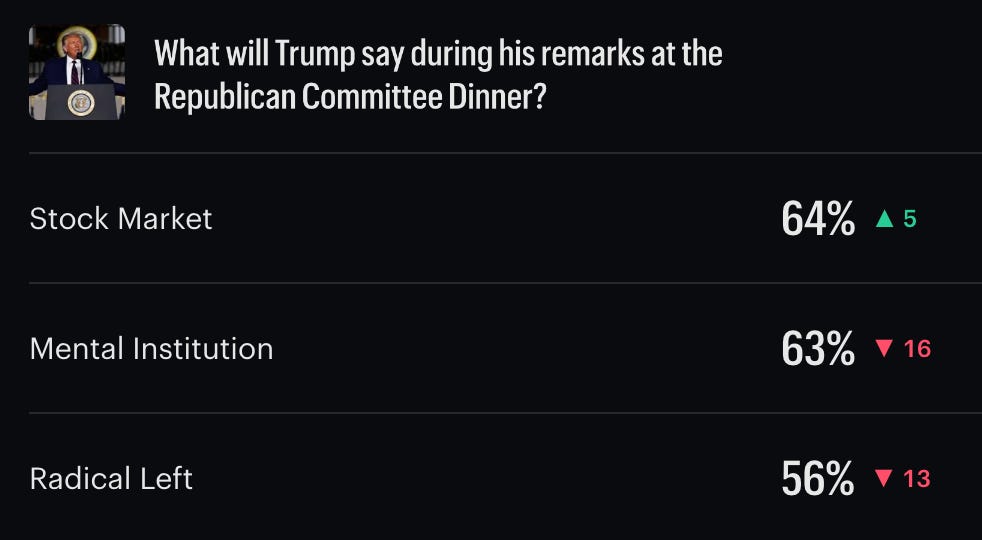

Prediction markets are not just about outcomes because you can close your position before the market resolves. For example, you may agree with the 56% of people who are currently betting that Trump says the phrase “Radical Left” at the upcoming Republican Committee Dinner. If you put your $56 where your mouth is and turn out to be right, you will be paid out $100 (a $44 profit). In other words you made a $56 bet at 1.79x odds.

However, if tomorrow the market becomes more bullish on this prediction and believers in the radical left mention market increase to 75% - you can close your position (for $19 profit).

I think this is neat because it’s like making two bets at once. The primary outcome oriented bet and a secondary but more meta-reputational bet on the agents aka insiders on the playing field.

We should want insiders to put skin in the game and move prices. A market that only reflects the views of the uninformed is simply a poll.

What kinds of information advantages and real‑world influence do we want to permit going forward? Ultimately we the people decide. If we don’t lean into frontier behavior then they will decide the rules for us.

If you imagine yourself as both a trader and a subject of these markets, wouldn’t you rather live in a world where you retain the ability to “bet on yourself”?